Last Updated on 2025-01-18 by Admin

A Collar (also known as a Protective Collar) is a popular options strategy that combines the use of a long position in the underlying asset, a covered call, and a protective put. The purpose of a collar is to limit potential losses on the underlying asset while also capping potential gains. This strategy is often used by investors who want to protect themselves from downside risk, but who are also willing to limit their upside potential in exchange for that protection.

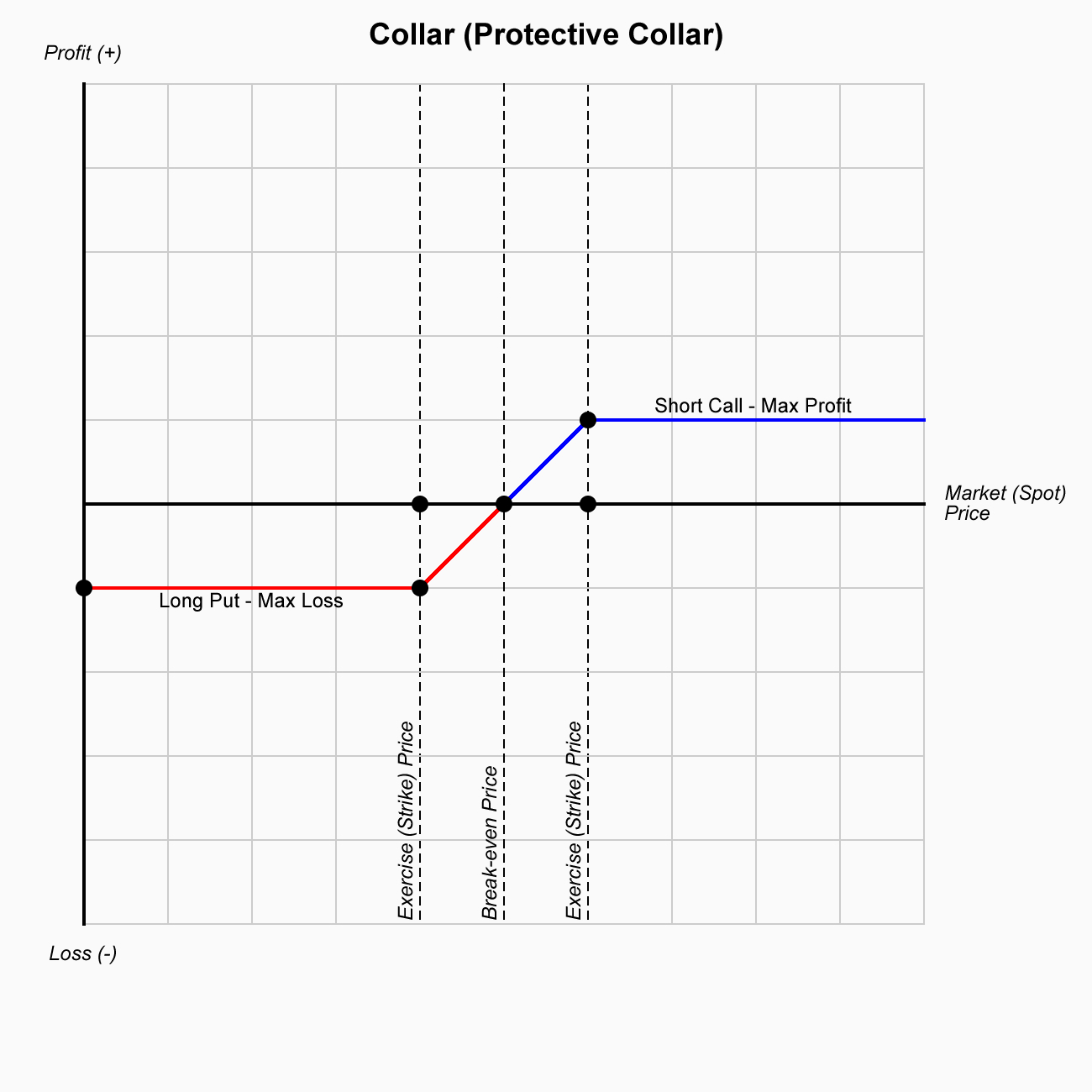

Pay-Off Diagram

Key Elements

- Long Position in the Underlying Asset: The investor holds shares (or another asset) that they are concerned about losing value in, but still want to retain some exposure to the asset.

- Selling a Covered Call: The investor sells a call option on the asset at a strike price higher than the current market price. This generates income through the premium received from selling the call, which can help finance the cost of buying the protective put. The covered call also caps the potential gains because if the price of the asset rises above the strike price, the investor will be forced to sell the asset at that price.

- Buying a Protective Put: The investor buys a put option on the same underlying asset at a strike price lower than the current market price. This put option provides downside protection, ensuring that if the price of the asset falls, the investor can sell the asset at the put’s strike price, thus limiting their potential losses.

Objectives

The collar strategy is used to limit downside risk while also capping upside potential. This strategy is suitable for investors who want to protect their gains or limit losses in a volatile or uncertain market but are willing to forgo unlimited potential profits in return for the protection provided by the put option.

Mechanics

The collar strategy typically involves the following steps:

- Hold the Underlying Asset: The investor owns shares or an equivalent amount of the underlying asset (e.g., stocks, ETFs, etc.).

- Sell a Covered Call: The investor sells a call option with a strike price higher than the current market price of the underlying asset. This allows them to collect a premium upfront, which can help offset the cost of purchasing the protective put.

- Buy a Protective Put: The investor buys a put option with a strike price lower than the current market price. This limits the potential loss on the position if the price of the underlying asset falls significantly.

The protective collar limits both potential losses (through the protective put) and potential gains (through the sold call option). The cost of buying the protective put is partially or fully offset by the premium received from selling the call option, making it an affordable risk management strategy for some investors.

Example

Let’s consider an investor who owns 100 shares of a stock currently trading at $50 per share. The investor wants to limit potential losses but also wants to potentially profit from some upside movement. The investor decides to implement a collar strategy by selling a covered call and buying a protective put.

- Hold the Underlying Asset: The investor holds 100 shares of the stock at $50 per share.

- Sell a Covered Call: The investor sells a call option with a strike price of $55, expiring in one month, for a premium of $2 per share. The total premium received is $200 (since one options contract represents 100 shares).

- Buy a Protective Put: The investor buys a put option with a strike price of $45, expiring in one month, for a premium of $1 per share. The total cost of the put option is $100.

In this case, the investor is using the $200 premium from the covered call to help offset the cost of the $100 premium for the protective put. Therefore, the net cost of the collar strategy is $100 ($200 premium from the call minus $100 cost of the put).

Possible Outcomes

- If the stock price rises above $55:

- The investor will be obligated to sell the stock at $55 (due to the covered call). The stock is sold at the strike price of the call option.

- The profit from this scenario is limited to the difference between the initial stock price and the strike price of the call option, plus the premium received.

- For example, if the stock rises to $60, the investor sells the stock at $55, generating a $5 per share profit, plus the $2 premium from the call. The total profit is $7 per share.

- If the stock price stays between $45 and $55:

- The put option expires worthless, and the investor keeps the stock. The call option also expires worthless, so the investor keeps the premium from the call ($200) but has no obligation to sell the stock.

- In this scenario, the investor’s effective profit is the premium received from selling the call ($200), minus the cost of the put ($100), for a net gain of $100.

- If the stock price falls below $45:

- The put option is exercised, and the investor is able to sell the stock at $45 (the strike price of the put option).

- The maximum loss is limited to the difference between the current stock price and the put strike price, minus the premium received from the call. For example, if the stock falls to $40, the investor will sell it at $45, avoiding further losses below that price. The maximum loss would be $5 per share (from the initial price of $50 to the put strike price of $45), but this is offset by the $2 premium received from the call, so the net loss is $3 per share.

Risk/Reward Profile

- Maximum Profit: The maximum profit in a collar strategy is limited to the strike price of the sold call (minus the purchase price of the stock) plus the premium received from selling the call. If the price of the underlying asset rises above the call strike price, the investor will be forced to sell the asset at the strike price, and any further price increases are not captured.

- Example: If the stock rises to $60, the maximum profit is $55 (strike price of the call) minus the $50 purchase price of the stock, plus the $2 premium received from the call, for a total maximum profit of $7 per share.

- Maximum Loss: The maximum loss occurs if the price of the underlying asset falls below the strike price of the put, but the loss is capped at the difference between the stock’s current price and the put’s strike price (less the premium received from selling the call).

- Example: If the stock falls to $40, the maximum loss is $50 (purchase price of the stock) minus $45 (put strike price), plus the cost of the put premium ($100). This results in a maximum loss of $300 (or $3 per share), which is a limited loss compared to the potential loss without the collar.

- Breakeven Point: The breakeven point occurs at the current price of the stock minus the premium received from the call option, plus the cost of the put option.

- Example: If the stock is at $50, the net premium received from the call is $200, and the cost of the put is $100. The breakeven point is $50 (current stock price) – $2 (call premium) + $1 (put premium) = $49 per share.

Pros

- Downside Protection: The protective put provides downside protection, limiting potential losses if the price of the underlying asset falls sharply.

- Income Generation: The premium received from selling the call option generates immediate income, which can help offset the cost of the put option or contribute to the overall return.

- Defined Risk/Reward: The collar strategy provides a defined risk and defined reward. Investors know the maximum potential loss and gain upfront, which can help with risk management and planning.

- Cost-Effective: In many cases, the premium received from selling the covered call can offset the cost of buying the protective put, making this strategy relatively inexpensive for the investor.

Cons

- Limited Upside Potential: The collar strategy caps potential profits. If the underlying asset rises significantly above the call’s strike price, the investor will not benefit from the additional price increase. They are obligated to sell the asset at the strike price of the call option.

- Opportunity Cost: While the investor has limited downside risk, the strategy also limits the upside potential, which could be frustrating if the underlying asset performs very well.

- Complexity: The collar strategy can be more complex than simply holding the underlying asset, as it requires managing multiple options contracts (buying a put and selling a call) while maintaining a long position in the underlying asset.

- Transaction Costs: There can be significant transaction costs associated with implementing the collar, especially when buying and selling options contracts frequently.

When to Use

- Protect Gains: The collar is ideal for investors who have gained a substantial amount of value in an asset and want to lock in profits while still having limited exposure to downside risk.

- Uncertain Market Conditions: This strategy is well-suited for times when the investor expects volatility in the market but is unsure of the direction. It provides a hedge against large losses while still allowing for some upside potential.

- Neutral to Moderately Bullish: The investor believes that the asset’s price will stay within a specific range or rise moderately, but they want to limit losses if the price falls.

Conclusion

The collar (protective collar) strategy is a risk management tool that allows investors to protect against downside risk while capping potential upside gain. By combining a long position in the asset, selling a covered call, and buying a protective put, the collar provides a defined risk/reward profile. This strategy is useful for investors looking to hedge their positions in volatile markets, protect gains, or generate income through options premiums, while also being willing to limit potential profits. The strategy works well in markets with uncertainty or volatility and is especially attractive to investors with neutral to slightly bullish outlooks.